A few months ago, someone shared a screenshot in one of our community chats. He had just sent money from Nairobi to his family in Chennai. Transfer went through fine. But when his mother received it and converted to rupees at her bank, the effective rate he got was nearly 8% worse than the mid-market rate. That was not a fee disclosed upfront. It was buried in the spread.

He had used his bank. And the bank had quietly taken KES 4,000 on a KES 50,000 transfer, dressed up as a competitive exchange rate.

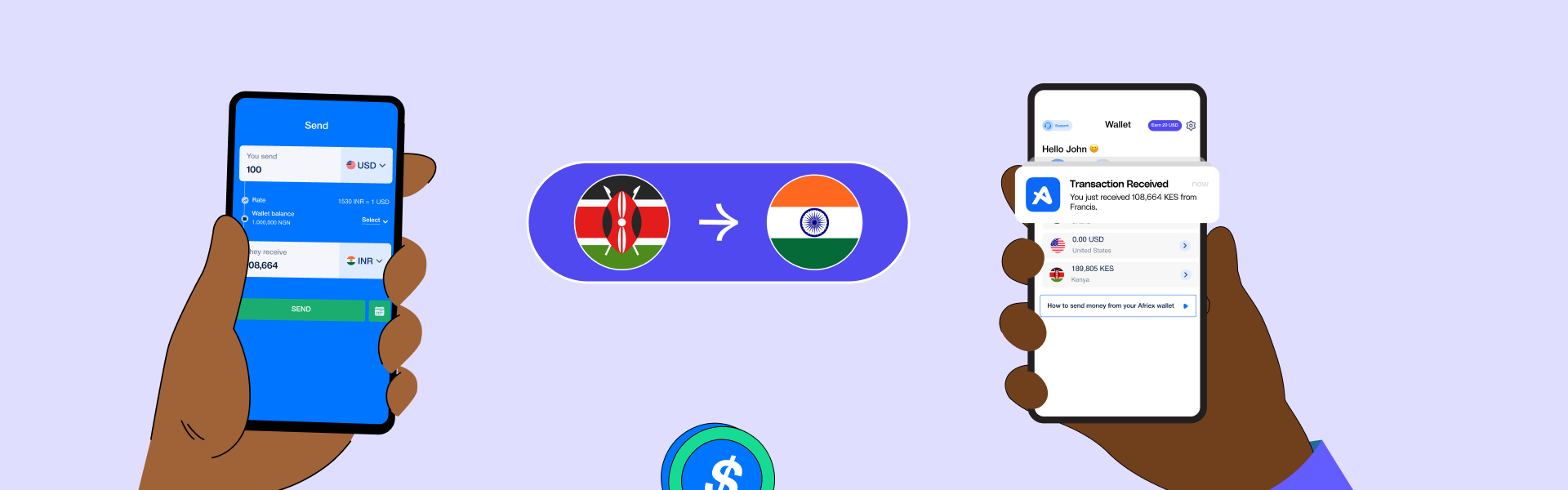

The Kenya-India corridor is bigger than most people realize. There are roughly 80,000 to 100,000 Kenyans of Indian origin, many of whom regularly support family members back home or pay business suppliers across the subcontinent. Kenya and India have over $1.5 billion in annual bilateral trade as of 2025, according to data from the Kenya National Bureau of Statistics. That is a lot of money moving between two countries, and most of it is still flowing through channels that quietly extract value from senders.

I want to be genuinely useful here, so let me walk through what I have actually seen work on this corridor.

Why the Kenya-India Corridor Is More Complex Than It Looks

On paper, sending money from Kenya to India sounds simple. You have a source currency (Kenyan shillings, KES), a destination currency (Indian rupees, INR), and a range of digital services claiming to make the process fast and easy. But a few things complicate this corridor specifically.

India has strict foreign exchange controls. The Reserve Bank of India (RBI) regulates inbound transfers under the Foreign Exchange Management Act, known as FEMA. Not every international transfer service can deliver directly to Indian bank accounts. Some route through intermediaries, which adds delay and sometimes additional costs. Before you send, confirm the service you are using has an RBI-regulated banking partner on the receiving end. Any service that cannot explain this clearly is worth questioning.

The spread problem is also pervasive on this corridor. KES/INR is not a heavily traded currency pair like EUR/USD or even USD/KES. That gives services pricing this conversion more room to embed a markup in the exchange rate itself. I have seen spreads ranging from 1.5% on the better end to over 7% on the worse end. On a KES 50,000 transfer, a 7% spread is over KES 3,500 extracted before the money even arrives.

Transfer limits are a third thing to watch. If you are sending business payments, some consumer-focused apps cap individual transfers at amounts that force you to split a payment across multiple transactions. That creates compliance documentation on the Indian receiving side and can delay settlement by days.

What to Have Ready Before You Send

Most of this is administrative, but missing one item delays your transfer by days.

On the Kenya side: your national ID or passport, your M-Pesa number or bank account for funding the transfer, and your KRA PIN if the service asks for tax identification on larger amounts.

On the India side: the recipient's full bank name, account number, and IFSC code. This last one trips people up. The IFSC code is India's equivalent of a sort code or routing number. Every branch of every Indian bank has a unique IFSC code. If the recipient gives you only their account number, the transfer cannot be processed. Make sure you get the IFSC code in advance. Recipients can find it on their bank statement, in their bank's mobile app, or by calling the branch directly.

If you are paying a business supplier in India rather than a personal recipient, you may also need their GST registration number and a brief description of what the payment is for. This is not always required but is increasingly asked for on amounts above certain thresholds as India tightens foreign payment documentation under FEMA. Get this from your supplier before you initiate the transfer, not after.

What the Stablecoin Shift Means for This Corridor

Something is changing on the infrastructure side of Africa-India payments, even if the app interface looks the same to you as a sender.

Several Africa-focused payment companies are now settling their cross-border payments using stablecoins, specifically USDC and USDT, on the back end. NALA, the East African fintech, just secured a $50 million credit facility to expand its stablecoin-powered payment rails across corridors including those connecting East Africa to South Asia. Grey processed over $61 million through stablecoin-settled business transfers in just four months. Esca Finance, which processes between $75 million and $120 million monthly across African corridors, recently brought on MANSA (a Tether-backed liquidity provider) to enable same-day settlements.

What this means practically for someone sending from Kenya to India is that the technology powering the transfer is getting faster and cheaper, even if the front-end experience looks familiar. Stablecoin settlement allows payment companies to move value in near real-time without needing to pre-fund local accounts in every destination country. That reduces the cost of running a corridor, and well-run companies pass that saving along in better rates or faster delivery times.

If you have been using a service that felt slower or more expensive than it should be, it is worth reassessing in 2026. The infrastructure has shifted considerably in the past 18 months.

How Long Should It Take

A reasonable benchmark for this corridor right now is 1 to 24 hours for most digital transfer services. Many complete in under two hours. If your transfer is taking more than 48 hours, something has likely been flagged for manual review. That is not unusual on first-time transfers or on amounts above a certain threshold. The solution is to have your identification documents ready to submit if the service contacts you and to respond quickly. Delayed responses extend processing times significantly.

Bank wire transfers on this corridor typically take three to five business days, occasionally longer if there is a public holiday in Kenya, India, or any country on the correspondent banking route.

A Note on Safety

This is worth stating directly: always verify the recipient's account details through a separate channel before sending. The most common fraud on payment corridors involves someone intercepting communication between a sender and receiver and substituting the fraudster's account details. If you are paying a supplier you have not used before, call them to confirm the account number and IFSC code verbally before initiating the transfer. A five-minute call can prevent a loss you cannot recover.

One more: no legitimate payment service will ask you to send money to a third-party account as a "verification transfer." If you see that request, it is a scam.

Where to Start

If I were sending money from Kenya to India today, I would open three apps, get a live quote from each at the same moment, and look at only one number: how many rupees the recipient would receive. Not the advertised fee. The amount received.

The KES/INR mid-market rate right now sits around 0.72 to 0.73 rupees per shilling, depending on the hour. Any service offering you noticeably less than that on a conversion is building its margin into your transaction. You are entitled to know that, and you are entitled to shop for better.

The good news is that competition on this corridor has grown. That benefits you. The tools exist to send money from Kenya to India the same day, at a transparent rate, with the recipient getting funds directly to their bank account. The only remaining question is whether you know what to compare before you send.

Now you do.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.png)

.png)