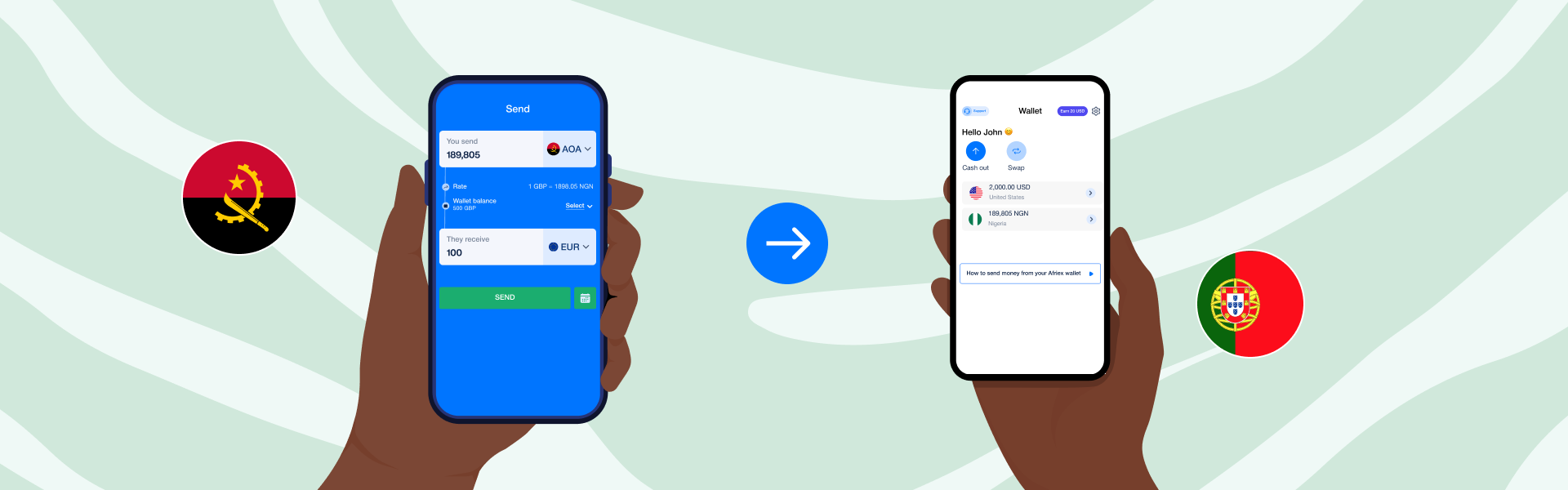

My team has processed thousands of cross-border transfers across African corridors, and the Angola-Portugal route is one of the ones that consistently surprises people. Not because it's complicated. Because how much money quietly disappears before it arrives.

Portugal is home to somewhere between 200,000 and 300,000 Angolans, making it the largest Portuguese-speaking African diaspora community in Europe. Many of them send money back to Luanda, Benguela, or Huambo every month. Some are sending to elderly parents. Others are covering school fees, medical bills, or supporting a business back home. The transfers are regular, the amounts are real, and the fees are far too high.

If you're navigating this corridor, whether from Portugal sending to Angola or from Angola sending to Portugal, this guide covers what actually works, what to watch out for, and why the cheapest-looking option is often not what it appears.

Why the Angola-Portugal Corridor Is Unusually Complicated

Most cross-border payment guides treat corridors like interchangeable plumbing. Send money from A to B, compare three apps, pick the cheapest. But Angola has some structural features that make this corridor different from, say, Nigeria to the UK or Ghana to Germany.

Angola's currency, the kwanza (AOA), is not freely convertible. The Banco Nacional de Angola (BNA), the country's central bank, controls foreign exchange. That means the official rate at which kwanza converts to euros is not set by the open market; it's managed. And like most managed exchange rate systems, there's often a gap between the official rate and what the market would price the currency at if left alone.

For people sending money from Angola, this creates a real practical problem. A bank wire might give you the official rate, which can be significantly worse than what you'd find on the street or through informal channels. But informal channels carry their own risks, particularly around regulatory compliance and the safety of large transfers.

The result is that many Angolans in Portugal have historically relied on a small number of traditional operators, MoneyGram and Western Union having long been the dominant players, or direct bank-to-bank wires. Both are expensive. According to World Bank data, sub-Saharan Africa remains the world's most expensive remittance region, averaging above 7% in transfer costs. Angola's corridors often sit at the higher end of that range.

What Most People Get Wrong: The Bank Wire Trap

The most common mistake I see is people defaulting to their bank.

It feels safe. The interface is familiar. Your bank already has your details, and sending a wire seems like a straightforward next step. But banks are consistently one of the most expensive options for international transfers, and the Angola-Portugal route is no exception.

Here is what a typical bank wire actually costs you. First, there's a flat fee, often ranging from 15 to 40 euros on the Portuguese side or the equivalent in kwanza on the Angolan side. Then there's the exchange rate margin. Most banks take 2.5% to 4% above the mid-market rate without telling you explicitly. If you're sending 1,000 euros, a 3% margin is 30 euros gone before the money even moves. Add the flat fee and you're potentially losing 50 to 70 euros on a single transfer.

If you're sending regularly, that compounds fast. Three transfers a month at those rates is 150 to 200 euros per year in unnecessary costs. That's a month's worth of groceries for a family in Luanda.

There's also the speed problem. Bank wires to Angola can take 3 to 5 business days, sometimes longer if there's a correspondent banking check. For people waiting on money for urgent expenses, that delay matters.

The Options That Are Actually Worth Your Time

I want to be concrete about what's genuinely available for this corridor in 2026.

Platforms built specifically for Lusophone corridors. Because the Angola-Portugal route has real volume, a few specialist services have emerged that focus specifically on Portuguese-speaking corridors. These tend to offer competitive rates, local language support, and payout options that map more cleanly to how Angolan recipients actually hold money. They're worth investigating alongside the larger names.

Multicaixa and local wallet options. Inside Angola, Multicaixa is the dominant payment infrastructure, run by EMIS (Empresa Interbancária de Serviços). Many Angolans use Multicaixa Express, the mobile wallet attached to the Multicaixa network, for everyday payments. When evaluating any transfer service, check whether payout can land in a Multicaixa-linked account or the recipient's bank debit card linked to Multicaixa. That makes collection faster and avoids the recipient needing to visit a physical bank branch.

Stablecoin rails for business transfers. If you're transferring larger amounts, particularly for business purposes, the stablecoin route has matured significantly. African fintech platforms now let senders convert local currency to USDT or USDC, move it across borders, and convert to the destination currency at the other end, often with significantly lower spreads than traditional banking. This approach works better for amounts above 2,000 euros and for people comfortable managing a wallet interface. For regular family remittances, it adds complexity that isn't always worth it.

A Note on the Kwanza Rate

If you're sending from Angola to Portugal, the kwanza exchange rate is the biggest variable in your total cost.

The BNA officially manages the rate, but there are meaningful differences between what different service providers quote. Some providers use the official BNA rate. Others use a slightly different reference depending on their banking relationships and how they source euros. A 2% difference in the rate on a 500,000 kwanza transfer (roughly 500 euros at recent rates) is a 10 euro swing.

The practical implication: don't treat the kwanza amount as fixed when comparing services. Compare the euro amount that actually arrives in Portugal for a given kwanza input. That's the number that matters.

Also worth knowing: the BNA has historically imposed limits on individual foreign exchange transactions. These limits can affect large transfers or transfers that happen too frequently. If you're sending regularly, it's worth checking whether your chosen service has a relationship with a local bank that handles larger volumes without triggering transaction flags. Some services are better positioned for this than others.

For Businesses Sending Between Angola and Portugal

The corridor isn't just for personal remittances. Angola and Portugal have deep trade ties stretching back decades. There are Angolan businesses with suppliers in Portugal and Portuguese companies with operations or partners in Angola. B2B transfers between the two countries are common, and they come with an additional layer of complexity.

For business transfers, the requirements include commercial invoices, proof of the underlying transaction, and often prior approval from the Angolan side for transfers above certain thresholds. Portuguese banks are generally equipped to handle this, but the timelines are longer and the documentation requirements are real.

Fintech platforms built for business are increasingly useful here. They often handle the compliance documentation requirements, have relationships with local banking partners that smooth out the BNA-related friction, and provide transaction records in a format that works for corporate accounting. If you're running regular business payments on this corridor, it's worth setting up a dedicated business account with one of these platforms rather than routing everything through a traditional bank.

What to Have Ready Before You Send

Before your first transfer on this corridor, a few things speed up the process significantly.

You'll need the recipient's bank name and IBAN (for transfers landing in a Portuguese bank account), or the Angolan bank's SWIFT/BIC code plus account number for transfers landing in Angola. Most Angolan banks are connected to the SWIFT network; BFA (Banco de Fomento Angola), BIC (Banco BIC), and BAI (Banco Angolano de Investimentos) are the major names you'll encounter.

For compliance, transfer services typically ask for proof of identity on both sides for amounts above certain thresholds. Have your passport or national ID ready. Services may also ask the purpose of the transfer, which is standard practice and matters more for Angola given the BNA's oversight of outbound foreign exchange.

If the recipient is picking up cash rather than receiving a bank deposit, they'll need ID matching the name on the transfer. Confirm this in advance so they don't show up without the right documentation.

The Bigger Picture on Angola-Portugal Transfers

I'll be direct about something: this corridor is underserved relative to its actual demand.

There are hundreds of thousands of people moving money between Angola and Portugal every month. The digital infrastructure for doing it cheaply and easily has lagged behind corridors like Nigeria-UK or Kenya-USA simply because the volumes haven't historically attracted as much fintech attention. That's changing, but it means the options are more fragmented and require more active comparison than more mature corridors.

The 3% global SDG target for remittance costs is a long way off for Angola. Sub-Saharan Africa overall averages above 7%, and Angola's specific constraints around currency convertibility add to that. Until the market matures further, the practical advice is the same as it is for most underserved corridors: compare on every transfer, not just once. The best rate today may not be the best rate next month.

We built Afriex to reduce that friction for African corridors, and I'd encourage you to compare options across platforms to find what works for your specific needs on this corridor. What matters is that you're not leaving money on the table with every transfer.

The Angola-Portugal link is one of the older, deeper Africa-Europe connections. The people using it deserve payment infrastructure that reflects that.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.png)

.png)