English

Sending money across borders is more than just a financial transaction—it's an act of care, responsibility, and connection. For immigrants and members of the African diaspora, regularly sending money back home to Nigeria, Kenya, or Ghana is part of supporting loved ones, paying for education, covering medical bills, or investing in small businesses.

However, the amount you send isn't always the amount they receive. Many senders are unaware of the layered costs behind international money transfers—costs that quietly chip away at their hard-earned funds. These include not only visible service fees but also hidden charges, such as poor exchange rates, local deductions, or withdrawal fees on the recipient’s side.

In this guide, we’ll explore the real cost of remittances to Nigeria, Kenya, and Ghana, break down the mechanisms involved, and offer actionable advice to help you maximize your transfers and minimize loss.

When you send money internationally, the true cost includes:

The combination of these factors means that a $200 transfer might only result in $185 worth of value on the receiving end. Now, let’s go into them.

Transfer fees are the most visible part of sending money. These are often:

Some services may appear to charge “no fees,” but they often make up the difference by inflating exchange rates, a less transparent form of profit.

Most remittance platforms offering transfers to Nigeria now charge low flat fees (ranging from $0.99–$4.99). However, when sending USD, the funds are often received in Naira after bank conversion, leading to indirect costs if the bank uses a low FX rate.

Transfers to Kenya commonly go to M-Pesa mobile wallets, and platforms may charge percentage-based fees depending on the delivery method. Some providers waive fees for higher-value transfers, but hidden FX margins still apply.

Like Kenya, Ghana has seen a rise in mobile money usage. Transfer platforms may advertise “free transfers,” but again, watch the exchange rate closely.

Arguably the most costly and least transparent component of international transfers is the exchange rate markup.

Here’s what that looks like:

Over a $500 transfer, this 60 NGN gap equals ₦30,000 in lost value.

If the real rate is 1 USD = 150 KES, a provider may offer 1 USD = 143 KES. That’s 7 KES lost per dollar, or 1,400 KES lost on a $200 transfer.

When the mid-market rate is 1 USD = 12.5 GHS and the provider offers 12.0 GHS, you lose 0.5 GHS per dollar—equating to 100 GHS on a $200 transfer.

Here’s why it matters. Many users focus only on fees and forget to check FX rates, not realizing this hidden cost can exceed the visible fee multiple times over.

Even after you’ve covered all the sender-side costs, the recipient may not receive the full amount due to local deductions. These include:

While Nigeria allows USD inflows, most everyday users will withdraw in Naira, either at the bank or via bureau de change. Banks may use official rates that are lower than black market or mid-market rates, further reducing the final value.

M-Pesa has tiered withdrawal fees. A recipient withdrawing over 20,000 KES might pay 100–200 KES in charges. Also, some platforms charge a service fee when disbursing funds to M-Pesa wallets.

MTN Mobile Money and other services charge a cash-out fee (usually 1–1.5% of the amount), depending on how the funds are used. Bank transfers also may incur incoming remittance fees, even when sent through digital platforms.

Need money to arrive in minutes? You’ll likely pay for the convenience.

Many platforms offer:

Due to FX fluctuations and banking delays, some services charge extra for instant USD delivery. Sending in Naira may be faster, depending on the provider.

Mobile wallet systems (like M-Pesa and MTN Mobile Money) are typically real-time, but international remittance partners may introduce a lag or charge for instant disbursement.

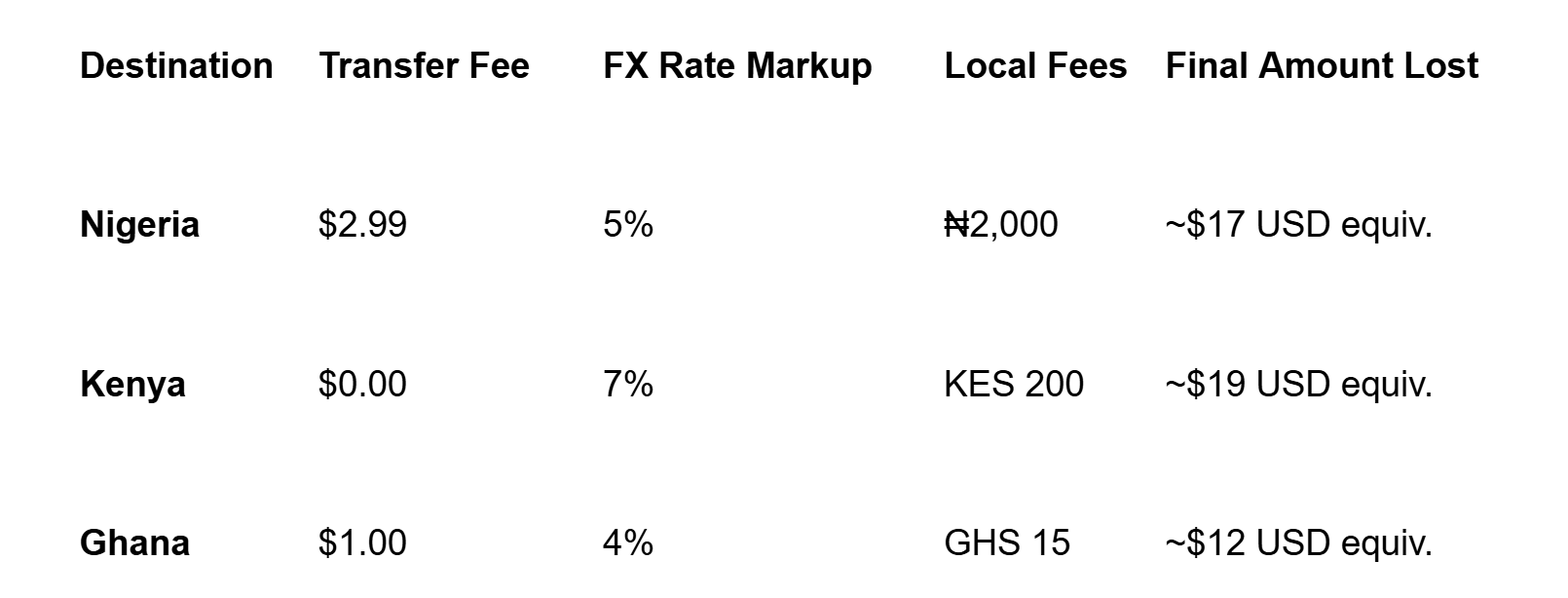

Let’s compare how much value is lost depending on the route and platform used. These are illustrative estimates:

Note: These values vary by provider and should be verified before sending.

Sending money is a regular habit for many people. These simple strategies can help you retain more value over time:

Remittances are a critical lifeline for millions of households. In 2023, Nigerians abroad sent over $20 billion back home. Kenya and Ghana each received billions in annual inflows as well. For many families, these transfers represent:

Yet, according to the World Bank, sub-Saharan Africa has the highest remittance costs globally, averaging 8–9% of the amount sent. The UN Sustainable Development Goal (SDG 10.c) aims to reduce this to below 3% by 2030.

Transparency, fintech innovation, and financial education are crucial to achieving this.

Afriex was built to simplify remittances for immigrants and remote workers—especially those sending money to and from Africa.

With:

Afriex removes the guesswork and helps you maximize the value of every transfer. You know what you send, what your recipient will get, and how fast it’ll arrive.

Sending money to Nigeria, Kenya, or Ghana shouldn’t feel like a gamble. Yet between fees, exchange rates, and receiving-end deductions, many people lose more than they realize.

Understanding the true cost of remittances gives you the power to make smarter decisions. Compare rates, track real-time FX values, and choose platforms that prioritize fairness and transparency.

Your money matters. Your family matters. And every dollar (or Naira, Cedi, or Shilling) should go as far as possible.

Looking for a trusted way to send money home without losing value?

Download the Afriex app today and join the mobile money movement that’s changing Africa’s future — one transaction at a time.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.png)

.png)