English

Remittances are more than just money transfers—they are the financial lifeline of African families. Across the continent, millions depend on funds sent by loved ones abroad for school fees, healthcare, food, housing, and small businesses. In fact, remittances often contribute more to household income than formal employment in many African countries.

Nigeria, Ghana, and Kenya consistently rank among the top three remittance-receiving nations in Africa. Together, they attract billions of dollars each year. But the rules for how money enters each country are not the same—and they directly affect how much value families ultimately receive.

This guide explores the current remittance policies in Nigeria, Ghana, and Kenya, breaking down what senders should know and how Afriex helps you navigate these rules easily.

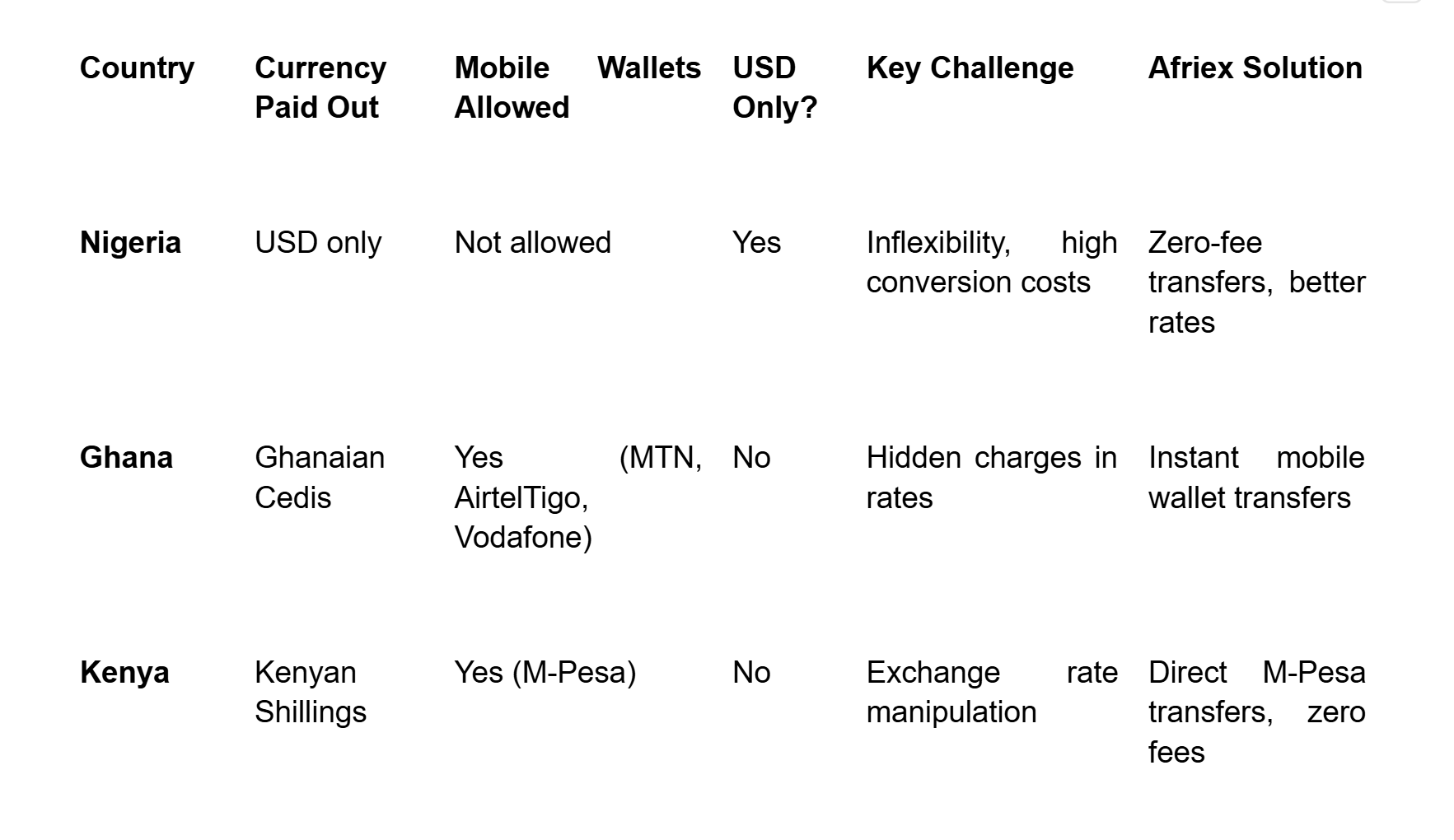

Nigeria receives over $20 billion annually in diaspora remittances, making it Africa’s largest market. However, its remittance space is also one of the most tightly regulated.

For many Nigerians, these rules create extra steps. A mother receiving money for her child’s school fees in Lagos might first pick up USD, then find a bureau de change to convert it into naira. That process often comes with long queues, poor exchange rates, and extra stress.

Afriex makes this easier by offering real-time exchange rates and zero transfer fees, so your family receives the full value without losing money in conversions or hidden charges.

Ghana’s remittance inflows are steadily growing, driven by a strong diaspora presence in Europe and North America. Unlike Nigeria, Ghana allows far more flexibility in how funds are received.

For most Ghanaian households, the ability to receive money straight into a mobile wallet is a game-changer. A grandmother in Kumasi can receive money in seconds and use it immediately to pay bills, buy groceries, or even send part of it to another relative—all without stepping into a bank.

Afriex integrates seamlessly with Ghana’s mobile wallet ecosystem, so funds arrive instantly and with zero fees, ensuring families enjoy convenience without hidden costs.

Kenya is globally recognized as the birthplace of mobile money innovation, thanks to M-Pesa. Its remittance policy reflects a focus on financial inclusion and security.

For a father in Nairobi, receiving remittances through M-Pesa means he can pay school fees, buy fuel, or shop at local markets without ever touching cash. The convenience is unmatched compared to traditional banking.

Afriex connects directly to M-Pesa, offering instant wallet transfers with zero fees. Families avoid long delays, poor rates, and unnecessary charges.

Though each country has different rules, one theme is consistent: senders lose money to fees and poor rates, while families bear the burden of limited access.

Afriex solves this by offering:

With Afriex, you can send to Nigeria, Ghana, or Kenya smarter and cheaper.

Sending money home should not be complicated. But remittance policies in Nigeria, Ghana, and Kenya mean that the method you choose matters. From Nigeria’s dollar-only rules, to Ghana’s mobile wallet adoption, to Kenya’s M-Pesa dominance, each country has a different path for receiving funds.

Afriex helps you cut through the complexity with a single solution: zero-fee, instant transfers at real rates. No hidden charges. No stress. Just money moving the way it should.

Download Afriex today on your iOS or android and send smarter—because every dollar, cedi, and shilling counts.

Remittance policies, exchange rates, and banking regulations in Nigeria, Ghana, and Kenya are subject to change. Always verify the latest requirements with official government or financial institutions before making transfers.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.png)

.png)