When I was building the early version of Afriex, I used to get a specific look whenever I mentioned stablecoins in the same breath as sending money to Nigeria. The polite version was: "that sounds complicated." The honest version, usually from someone's uncle, was: "my mother isn't going to use crypto."

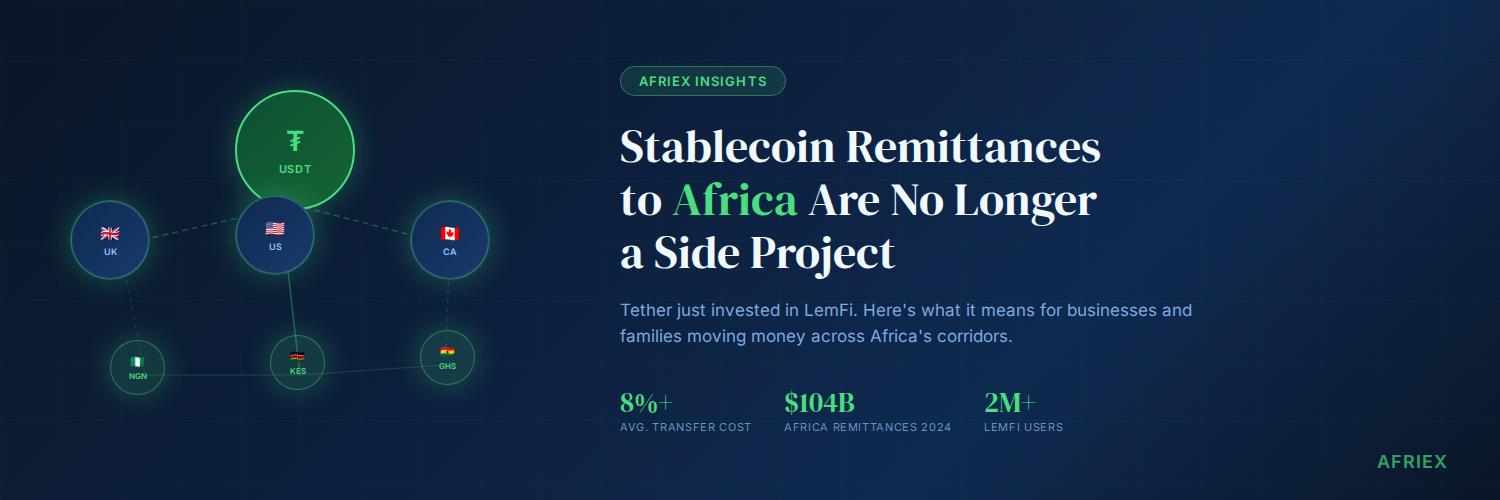

Those reactions were not wrong in 2021. But recently, we have seen a significant shift. Tether, the company behind USDT, the world's largest stablecoin by trading volume, has begun making direct strategic moves to integrate its infrastructure into established financial platforms serving the African diaspora across the UK, US, and Canada.

These are not "crypto apps." These are platforms where a cousin in London can open an account, load it with pounds, and family in Lagos gets naira in a bank account the same day.

This strategic direction represents a line in the sand. Stablecoin-powered remittances to Africa are no longer something you track on a crypto Twitter feed. They are being sewn into the financial infrastructure that real people use every day.

I want to work through what this actually means for businesses and families moving money between Africa and the rest of the world, especially right now when the naira is under serious pressure and the cost of getting payments wrong is higher than it has been in years.

How Stablecoin Infrastructure Is Rebuilding the Remittance Layer

The majority of diaspora remittance products work the same way on the surface: you send from your home country, and the recipient receives in local currency. The impact of major stablecoin issuers getting involved is found in the settlement layer underneath.

Right now, the majority of remittance transactions on African corridors move through chains of correspondent banks. Each hop adds cost. Each intermediary takes a margin. The result is that the average cost of sending $200 to Sub-Saharan Africa still sits above 8 percent, according to the latest World Bank data. That is more than double the 3 percent target the UN set for 2030, and we are four years out from that deadline.

USDT collapses that chain. Instead of moving value through five intermediaries, the transaction settles on a blockchain in seconds. The receiving side converts to local currency at the point of disbursement, which means the platform controls the FX conversion and can price it competitively rather than marking it up at every hop.

When major stablecoin infrastructure is plugged into that pipe, it is not a small signal. Tether processes more dollar-equivalent transactions globally than many mid-tier central banks. Plugging that capacity into platforms with millions of African diaspora users is the kind of integration that shifts market dynamics.

Why the Naira Situation Makes This More Urgent

The timing of this trend is not coincidental. As of this week, the Nigerian naira is at or near a record low against the dollar. Reuters and Bloomberg both reported on the naira's deterioration over May 18 and 19. The Central Bank of Nigeria has been intervening, raising rates, and managing FX supply, but the underlying pressure from import demand and constrained dollar supply persists.

I have watched this dynamic long enough to know what it does to the real cost of transfers. When I look at what a Nigerian business owner or a family depending on diaspora support is actually experiencing, every percentage point in transfer costs matters more in this environment than it did two years ago.

A $500 remittance sent through a channel with an 8 percent effective cost, once you add up the stated fee plus the exchange rate spread versus mid-market, arrives with the purchasing power of roughly $420 in practice. That gap is significant for a household budget. For a business moving $50,000 in supplier payments, it is a material cost line that belongs in your finance conversation, not in a footnote.

Stablecoin rails do not solve naira volatility. Nothing in the payment infrastructure solves what is fundamentally a macroeconomic problem. But they do address the cost side, the intermediary fee stack, far more aggressively than any other mechanism I have seen reach real-world scale. That is worth paying attention to.

The Business Case Is Different from the Family Remittance Case

Most of the public conversation about remittances focuses on household transfers. Families. Someone in Atlanta sending $200 to their parents in Ibadan.

The business case is less discussed and, in my experience, where the most painful inefficiencies sit.

A Lagos-based importer sourcing goods from a US or European supplier has to navigate dollar procurement at whatever rate the market will give, often with fees layered on top. A Nairobi manufacturer buying industrial components from China is running the same problem with different currencies. A Ghanaian startup paying a contractor in Toronto is navigating compliance requirements that make even a small international transfer feel like filling out a visa application.

For these businesses, stablecoin payment infrastructure offers something more useful than cost savings alone: predictability. When you hold USDT on a compliant platform, your treasury position is not moving against you while you wait for a wire to clear. You can pay an international invoice from that balance on the same day without scheduling a bank wire three business days in advance. For a small or medium-sized business managing cash flow tightly, that operational difference is significant.

The businesses I have seen navigate African payment corridors most effectively in the last two years share a specific habit: they have separated the currency they transact in from the currency they hold day-to-day. Dollar-stable instruments, including USDT on regulated platforms, are central to how they do that.

Three Questions About Your Current Payment Costs

When businesses come to me trying to figure out whether their payment setup is working, I start with the same three questions.

- What is your all-in cost per corridor, not just the stated transfer fee? Most businesses calculate the fee their bank charges for a wire. They do not calculate the exchange rate spread between what they paid and the mid-market rate that day. That spread is often 2 to 4 percent on its own, invisible in the transaction record but very visible if you run the numbers. On some corridors, especially into Nigeria right now, the combined cost is between 10 and 12 percent when you include every layer. That is a number worth knowing.

- How much operational time is your team losing to payment delays? A wire that takes three to five business days to arrive creates cash flow pressure that does not show up as a line item in your P&L but absolutely affects how you run your business. If your Nigerian supplier requires confirmed payment before releasing goods, and your wire takes a week, that is friction with a real cost.

- What happens to your operations if your primary payment channel gets disrupted? In the past year, African corridors have experienced rate freezes, temporary volume restrictions, and policy-driven disruptions that created short-term chaos for businesses that relied on a single channel. Redundancy matters. If stablecoin-enabled platforms are part of your corridor toolkit, you have options when traditional rails lock up.

Running those three questions across your actual payment data will tell you more than any product comparison can.

What the PAPSS Expansion Adds to This

Integration with stablecoins is not the only payment infrastructure development worth tracking right now. Earlier in May, PAPSS, the Pan-African Payment and Settlement System, announced a partnership with BCEAO, the central bank for Francophone West Africa, to bring eight West African nations into the continental settlement network.

PAPSS operates at the interbank layer, a layer below what most fintech products touch. Its purpose is to allow transactions between African countries to settle in local currencies rather than converting through USD or EUR intermediaries first. A payment from a Lagos business to a supplier in Abidjan that currently converts through dollars can, as PAPSS scaling progresses, move directly in naira-franc equivalents.

The timeline for this to reach the average Nigerian or Ghanaian business is not immediate. Banking integration takes time, and the eight new WAEMU nations are in early stages of onboarding. But the directional signal is clear: Africa's payment infrastructure is being rebuilt at the continental level, not just optimized at the edges.

For businesses thinking about their payment strategy beyond the next quarter, watching both the stablecoin layer and the PAPSS layer matters. They address different parts of the cost and friction stack, and they are both moving in the same direction.

What to Do About It

The practical response to all of this is not to start learning about blockchain. If blockchain is how this gets explained to you, that is the wrong starting point.

My honest advice is: find out what your payments are actually costing you.

Pull the last 90 days of international transfers, calculate the all-in effective exchange rate you received on each one compared to the mid-market rate on those dates, and add the total fees. If you are paying above 5 percent on any major corridor consistently, that is a cost problem with available solutions, not an unavoidable cost of doing business.

From there, compare your options. Stablecoin-enabled platforms, including some that look and behave like any other fintech app, are now processing real volumes on Africa's major corridors.

The third step is building redundancy into your setup. One channel is a vulnerability right now. Having a backup rail for your highest-volume corridors, whether that is a stablecoin platform, a regional fintech, or a second banking relationship, is the kind of operational discipline that looks like overhead until the day you need it.

Africa's payment infrastructure has been improving faster in the last three years than in the previous decade. The businesses that benefit most from that improvement are not the ones who understand the technical details. They are the ones who review their actual costs every quarter, stay curious about alternatives, and do not assume that their current setup is still the best available option.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.png)

.png)